In Malaysia and Indonesia, Takaful insurance penetration remains far below its potential - despite strong demand seeking ethical, Shariah-compliant protection. The challenge has never been demand. It’s been distribution.

Traditional agent-led models, while trusted, have limits in scale and efficiency. Fully digital models, meanwhile, often clash with regulators who insist on agent involvement, Shariah oversight, and physical documentation. This leaves a gap - one that Agent-Guided Digital Distribution (AGDD) is uniquely designed to fill.

Here’s how AGDD works in a compliance-friendly way:

- Agent at the centre – Every policy still begins and ends with a licensed agent. Customers do not complete the purchase online; instead, they fill the digital form first.

- Remote face-to-face meeting – The agent then schedules a compliant advisory session, conducted remotely if needed, ensuring suitability and proper disclosure.

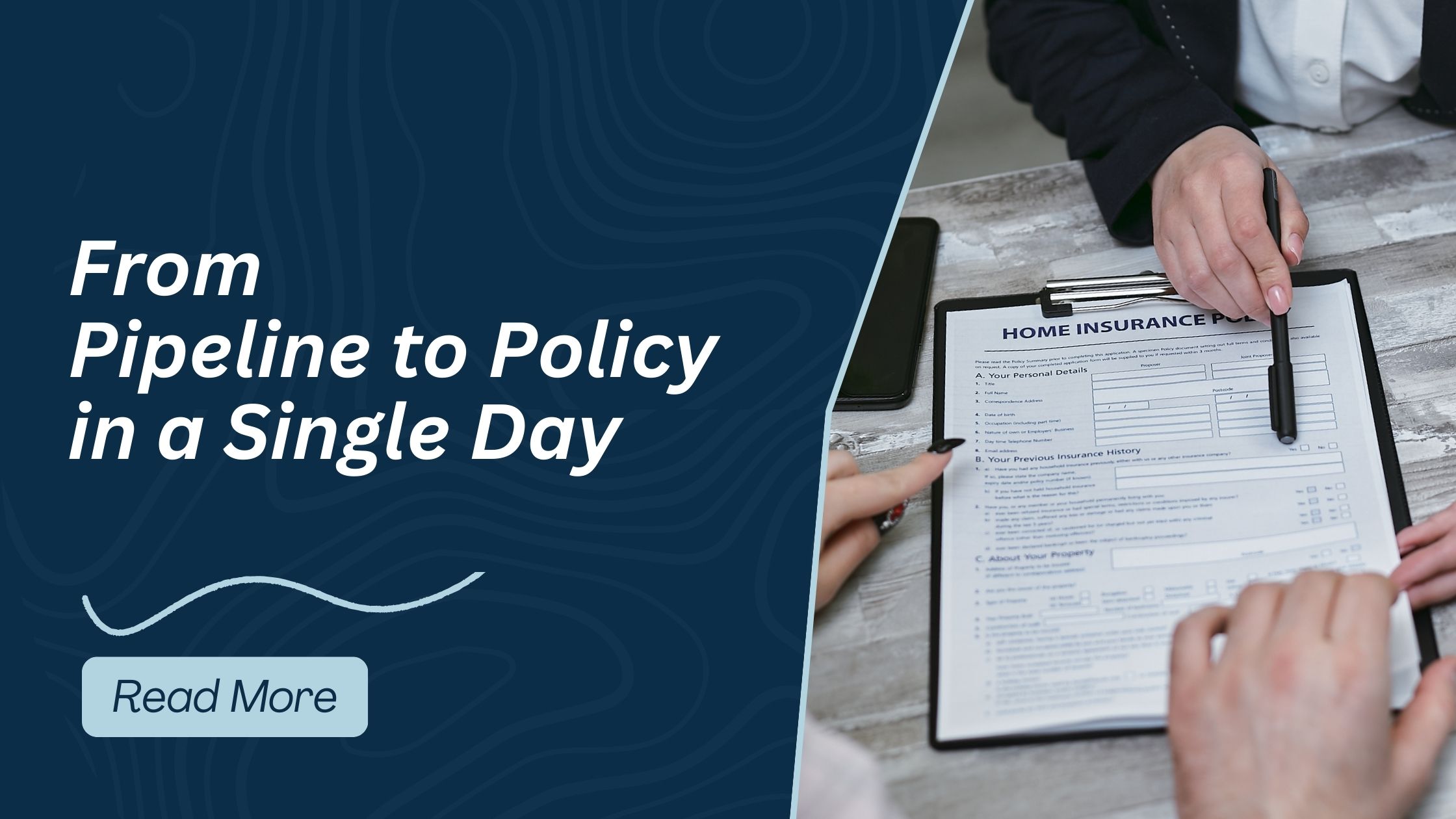

- Wet signature + physical document collection – Final paperwork is signed physically, with the insurer’s courier service collecting documents directly from the customer.

The result? Digital efficiency, traditional compliance.

For regulators, AGDD is not a digital threat. It avoids the “fully digital license” trap by keeping agents accountable and documents physical. For insurers, it expands reach and reduces drop-offs. And for communities, it bridges the gap - letting families in rural Kelantan or Sulawesi get protection without navigating city offices.

Imagine the impact:

- An agent who used to close 8–12 policies per month can now achieve 30+.

- Customers enjoy digital convenience without compromising on trust or compliance.

- Regulators see inclusion rise while maintaining Shariah integrity.

Takaful doesn’t need to choose between tradition and technology. With AGDD, it can have both - and unlock one of the largest untapped growth opportunities in the Muslim world.

Here’s how AGDD works in a compliance-friendly way:

- Agent at the centre – Every policy still begins and ends with a licensed agent. Customers do not complete the purchase online; instead, they fill the digital form first.

- Remote face-to-face meeting – The agent then schedules a compliant advisory session, conducted remotely if needed, ensuring suitability and proper disclosure.

- Wet signature + physical document collection – Final paperwork is signed physically, with the insurer’s courier service collecting documents directly from the customer.

Do you see AGDD as the safest path for Malaysia’s Takaful growth? Let’s hear your thoughts.